Retail therapy, anyone?

Pressures from employment, inflation and consumer behavior suggest a diverging outlook for retail

The past two years have seen a seismic shift in retail behavior. Supported initially with stimulus payments and generous unemployment benefits, consumers largely bought products rather than services. They avoided shopping in stores, opting instead for direct-to-home shipments or curbside pickup. This proved to be a boon to e-commerce and big-box retailers. Meanwhile, the restaurant industry quickly pivoted to online ordering and alternate delivery models just to survive. These changes were necessary at the time, but existing data suggests that some of the associated adaptations and new consumer behaviors are likely to stick around for the long haul. To understand the impact on the future of retail, we examine recent trends in retail employment, sales and pricing, as well as patterns of foot traffic in a variety of physical retail locations.

A “V-shaped” retail recovery?

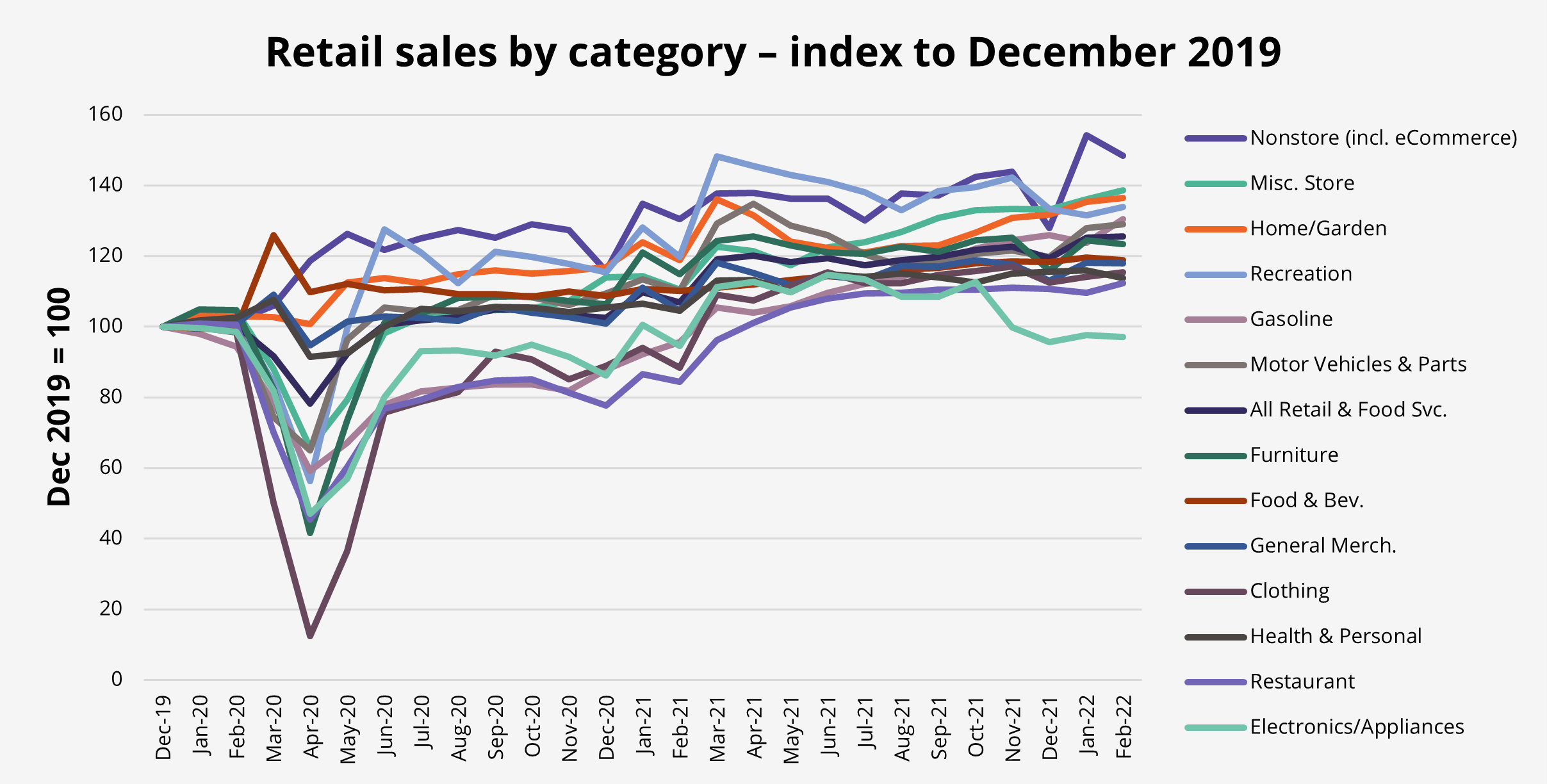

E-commerce sales have headlined the retail recovery, but most categories have resumed growth, with a few performing very well. With limited options during pandemic-related lockdowns, consumers turned to home improvement projects and outdoor activities—and away from buying clothes for going to work and spending their evenings out. This shift in behavior sparked sales growth at home and garden stores (which include building materials and yard equipment) of nearly 40 percent in February as compared to December of 2019, with recreational goods (including sporting and hobby goods) not far behind. Vehicle sales have also rebounded strongly. Clothing stores and restaurants have recovered more modestly from a deeper drop, but are now back in positive territory. Only electronics and appliances stores have failed to make a full recovery, doubtless due to their susceptibility to e-commerce.

Figure 1: Recovery in retail sales

Note: Seasonally adjusted

Source: US Census Bureau

Erik Edeen, Principal and Director of Operations in Avison Young’s Tri-State Investment Sales office, points to the experiential component of the various sectors and how it impacts their respective recovery. “For most people, it’s fun to go out to eat and to shop for home and garden items or recreational goods,” he says. “For products like gasoline, we have to have them, and the experience is all about speed and convenience.” The clothing and electronics sectors have recovered more slowly because the online customer experience can be superior to the in-person one. “Supply chain issues accentuate this,” Edeen says. “Consumers don’t want to show up to a store to get specific electronics or appliances, only to find out it’s not in stock.”

Will employment support continued growth?

Recovery in retail employment, on the other hand, has generally lagged behind sales. Employment at non-store and home & garden retailers is currently about 10 percent higher than it was before the pandemic. But in most other categories, it still trails December 2019 levels. At clothing and electronics/appliances stores, the slow recovery matches relatively slow sales growth. But in other sectors, such as restaurants and motor vehicles, employers are still struggling to hire workers back. In these sectors, labor market challenges could hinder faster recovery.

Figure 2: Retail employment recovery

Note: Seasonally adjusted

Source: US Bureau of Labor Statistics

Edeen points to another possible factor influencing the sluggish employment recovery in some subsectors. “As more stores seek to improve the experience by using physical retail as a showroom with online fulfillment, they may also change their space in a way that requires fewer employees.” This could change talent requirements as well, with retailers making a subtle shift toward employees who can curate options and provide detailed customer support rather than simply managing in-store transactions.

The inflation factor

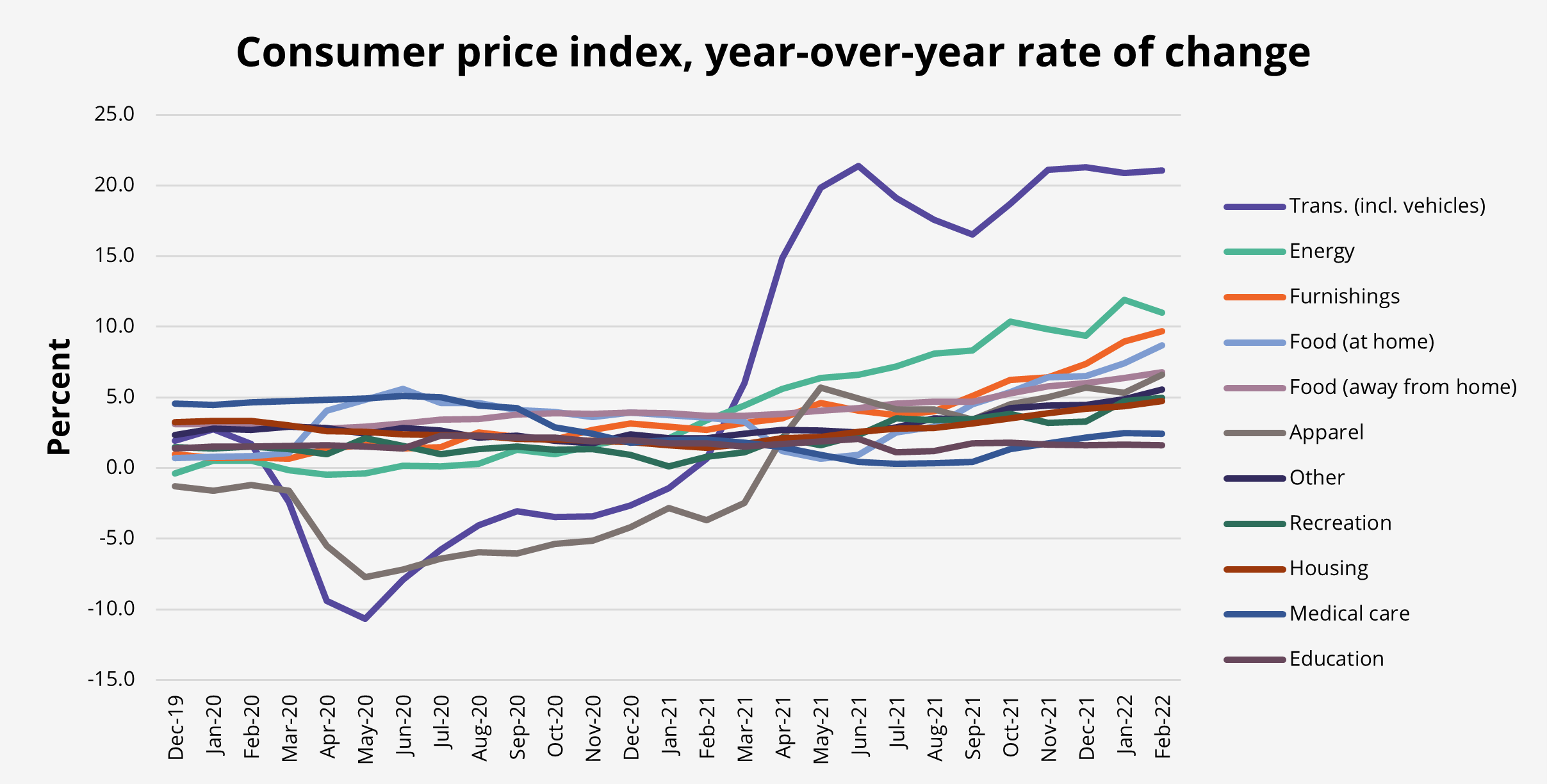

Inflation has been top of mind in recent weeks, advancing nearly 8 percent year-over-year in February. Core inflation (excluding food and energy) was somewhat lower, but still 6.4 percent. This prompted the Federal Reserve to raise interest rates by 25 basis points on March 16, a move long expected by economists. Transportation (especially vehicles) and energy (led by gasoline) have led recent pricing advances, but prices other retail categories have been steadily rising for several months.

Figure 3: Inflation on the advance

Note: Seasonally adjusted

Source: US Bureau of Labor Statistics

What might this mean for retailers? As we have already seen, the post-pandemic recovery in retail goods has been strong and fairly broad, but much has been driven by higher prices. There is good news for retailers of clothing and leisure goods, where sales growth has exceeded inflation by 4x (see Figure 4). Other categories have seen real growth as well, though most of the recovery at restaurants can be attributed to prices rather than increased volume. Changing preferences could mean that the strong sectors maintain real growth in the months to come. On the other hand, a rebalancing of customer behavior toward services could bring renewed energy to restaurants and other hospitality retailers.

Figure 4: Sales growth exceeds inflation

Note: Seasonally adjusted

Source: US Bureau of Labor Statistics, US Census Bureau

Brent Glodowski, Director, Retail Capital Markets Group at Avison Young, notes that inflation not only strains inventory costs for retailers, but also puts pressure on their leases. “Many lease escalation rates are pegged to the CPI,” he says. For example, a lease might have a provision for annual escalations of the greater of 2 percent or CPI. “A tenant who signed a lease two years ago probably assumed only a 2 percent annual increase each year, but this year that will not be the case. Large, national retailers with deep pockets might be able to weather this storm, but many smaller ones may reach a breaking point.” According to Glodowski, this might lead them to cut back on hiring plans and ask for accommodations from their landlords.

People are shopping again, but where?

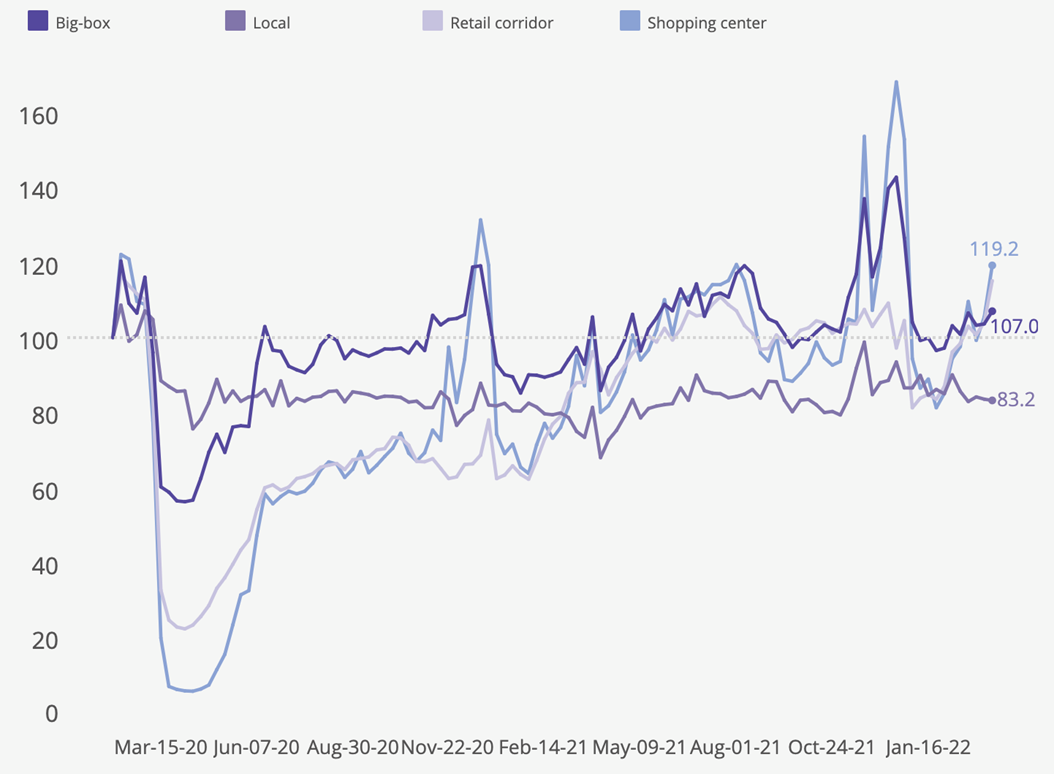

The pandemic transformed shopping habits, impacting how and where people make their purchases. It accelerated the adoption of direct-to-consumer sales and delivery and interrupted normal patterns of movement. This ultimately changed where people shopped. According to Avison Young’s Retail Vitality Index, some of this change may stick—including in unexpected ways.

Figure 5 displays the relative “recovery” of foot traffic across a sample of representative retail locations in the United States as compared to a typical weekday prior to the initial wave of lockdowns in the spring of 2020. The initial drop in foot traffic is apparent across all categories, but is less pronounced among local retail (which consists largely of grocery-anchored centers and convenience stores). This is intuitive since people still needed food and essential items. But traffic has yet to recover fully at these locations, remaining about 20 percent below the pre-pandemic norm.

Meanwhile, visits to big-box locations (including home improvement stores and discount clubs) recovered to about 90 percent of normal by the summer of 2020. This is better than retail corridor (high-profile areas like Chicago’s Magnificent Mile and New York’s SoHo) and shopping center (malls and outlet stores) locations. By the spring of 2021, when vaccines became widely available, these three categories all gradually trended back up, albeit with pronounced dips that coincided with the Delta and Omicron waves. They are currently at or above “normal” levels of foot traffic, with visible spikes during holiday shopping seasons.

Figure 5: Retail foot traffic by category vs. typical pre-pandemic weekday

Source: AVANT by Avison Young, Orbital Insights

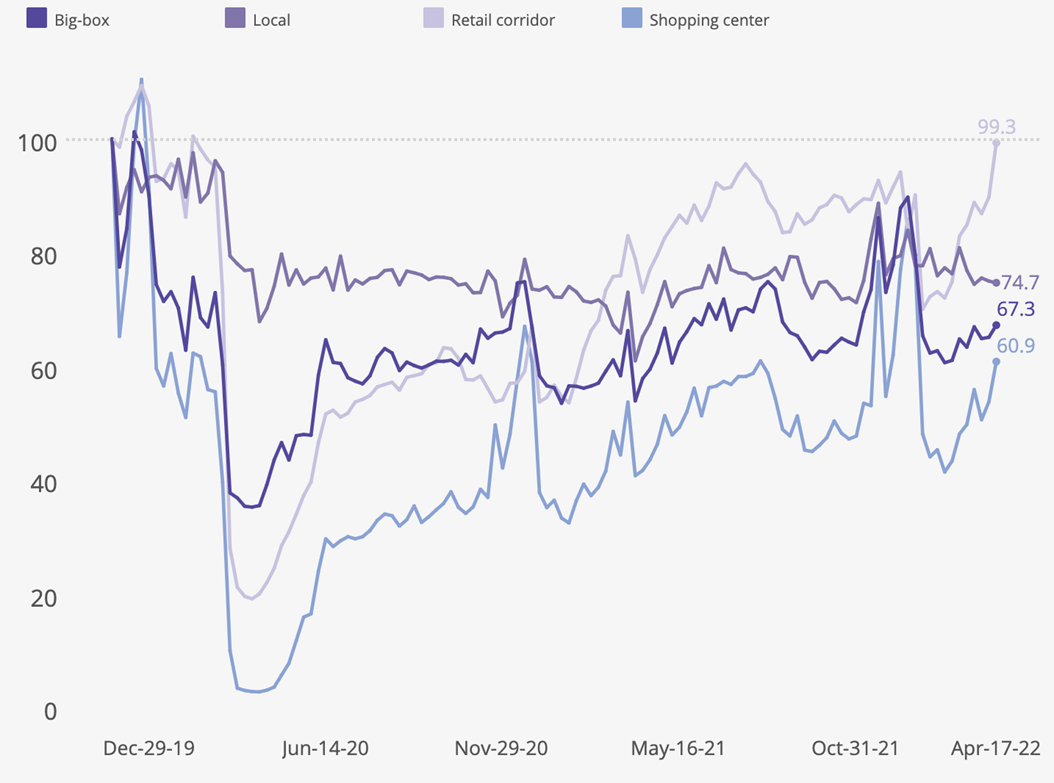

The story is incomplete, however, without examining the robust seasonal sales that many retailers depend on, particularly around the November/December holiday season. Figure 6 depicts foot traffic across the same retail sites as Figure 5, but this time with reference to Black Friday of 2019. It is apparent that, relative to this day of peak performance, most retailers have yet to attract comparable visits. The relative bright spot is the Retail corridor category, which retained about 90 percent recovery throughout the second half of 2021 and appears to be bouncing back quickly from the Omicron-induced dip early in 2022.

Figure 6: Retail foot traffic by category vs. Black Friday 2019

Source: AVANT by Avison Young, Orbital Insights

What’s next for retail?

This data tells us that, while conditions remain fluid, there are some indications about what might happen next in the retail sector:

- Big-box remains strong. Consumer behavior shifted toward products and away from services during the pandemic, which not only drove e-commerce, but also bulk items at big-box stores. The prospects for home improvement and warehouse club stores look bright, especially as prices rise and consumers seek discounts on groceries and household supplies. The stalling recovery in foot traffic at grocery-anchored centers may also indicate larger purchases in fewer trips, a pattern that could persist as knowledge workers keep spending more time at home in the era of hybrid work.

- E-commerce may have made a permanent dent in in-person sales of consumer goods, including electronics and clothing. These stores are still lagging in sales, employment and foot traffic compared to other retailers. Breaking newly established habits of online shoppers will be difficult.

- Retail corridors, restaurants and even shopping malls may have room for a resurgence. The months-long recovery in foot traffic at retail corridors and shopping centers suggests a release of pent-up demand for more experiential shopping; the immediate post-Omicron shift in sales toward services supports this. Restaurants, in particular, have struggled to stabilize employment, which has limited sales. As COVID concerns continue to wane, this constraint on growth will ease, enabling more experience-starved consumers to enjoy time out of the house.